Behind the barn walls at Milk Unlimited Dairy Farms is a sharp focus on protecting margins, controlling risk, and securing the farm’s long-term success — one well-managed day at a time. Kelly Cunningham shares his management philosophy and how Milk Unlimited has consistently maintained profitability for over 15 years.

Written by: Lucas Krueger, MS, PAS

KEY TAKEAWAYS IN THIS ISSUE OF TECHNICAL TOPICS:

- Margin protection—not milk price—is the real key to staying profitable year after year

- Managing risk across feed, milk, and cattle together gives a clearer picture of your bottom line

- You can’t protect what you don’t know—track your full cost of production monthly

- Lock in profits when they’re available to avoid the financial rollercoaster of market swings

- Forward contracts and options aren’t just for big farms—every producer can use them to control risk

- Consistent profitability sets the stage for future growth and generational sustainability

Outside the town of Atlantic, IA sits a 3,400 cow dairy farm that appears to be stereotypical of the large, commercial dairy farms in the Midwest. A year ago, results from the 2022 U.S. Census of Agriculture (produced every 5 years) showed that farms such as this, in a demographic of over 2,500 cows on site, accounted for over 44% of total U.S. milk sales, and farms of over 1,000 cows accounted for over 65% of the total. It is no secret that the survival and growth of dairy farms at scale require astute financial managers, but this month, I had the opportunity to interview and learn from one of the best, Kelly Cunningham, Managing Partner at Milk Unlimited Dairy Farms, LP. My goal was to gain a deeper understanding of Cunningham’s financial management philosophy and strategy, and to extract useful insights for dairy producers who are looking for answers amid today’s market uncertainty.

Cunningham’s management philosophy is rooted in margin protection. “At Milk Unlimited,” explains Cunningham, “we adopt a comprehensive approach to managing financial risk by evaluating feed risk, milk risk, and feeder cattle risk in tandem. This holistic analysis allows us to assess overall profit margins based on the individual price movements of feed, milk, and cattle. By avoiding emotional reactions and not chasing marginal gains in feed, milk, or beef prices, we have consistently maintained profitability for over 15 years. This strategic focus has been instrumental to our sustained success.”

“My goal is to take the highs out of the highs and the lows out of the lows.”

—Kelly Cunningham, Milk Unlimited

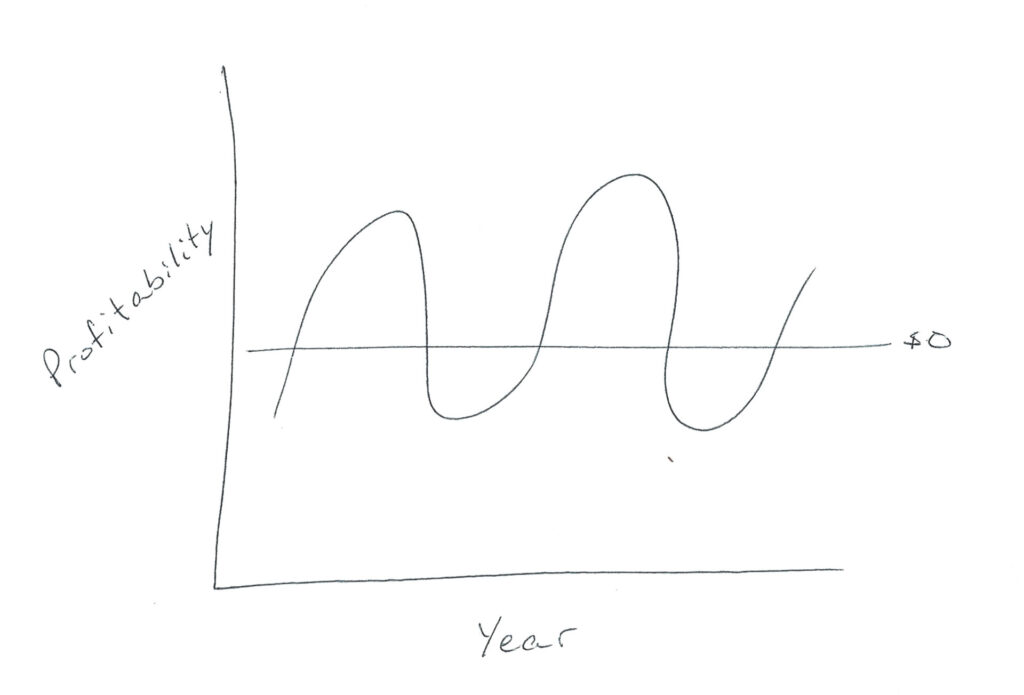

This philosophy, he explained, is critical for ensuring the long-term viability, growth, and success of his dairy. Milk Unlimited was built in 1998. The farm expanded in 2006 and again in 2012 to ultimately house the 3,400 Pro-Cross cows present today. To what does Cunningham attribute the dairy’s long record of success and profitability? “Avoid the losing years at all costs,” he says. As we first sat down together in his office, he drew a graph on a blank sheet of paper to illustrate a rollercoaster of high and low profitability years in the open markets. “My goal is to take the high out of the highs and the low out of the lows,” he explained. “Whenever the opportunity arises to secure profits, we take decisive action to lock in those gains, thereby minimizing overall risk exposure. In situations where profit margins are narrow, we prioritize preventing losses from escalating into larger ones.”

RIDING THE PROFITABILITY ROLLERCOASTER— this graphic captures the ups and downs dairy producers like Kelly Cunningham navigate as they manage margins.

Managing margins at Milk Unlimited is a meticulous and constant undertaking. In Cunningham’s eyes, financial control includes everything. “You must know your cost of production,” he says. He walked me through his financial worksheets, which detailed costs ranging from feed and labor down to diesel and electricity, and included interest and depreciation. He pointed out that until farm managers know their all-in cost of production, they cannot know or project their margin, which is the difference between milk price received and total costs. He reminded me that it is very common for dairy farmers or managers to meet with their accountant annually, and that can be a great place to start. In Cunningham’s eyes, however, many managers fall short of truly engaging with their itemized costs of production. By updating and monitoring costs monthly, dairy farm managers have much improved clarity and certainty about the margins that are in front of them in upcoming quarters. With that clarity, managers can begin to protect their margins through milk and feed contracts. Importantly, even small dairies can know their cost of production.

Cunningham gave me a detailed view of the vehicles he uses to control margins. By comparing current prices with historical prices, he recognizes when milk, corn, or soybean meal are historically high or low in price. Through his analysis with consultants at CIH, he then projects his profit margin per cow per day. He takes action to secure that margin through a combination of forward contracts, call and put options, and physical contracts on feed. Trading through Commodity & Ingredient Hedging (CIH) with a brokerage account at Archer Daniels Midland, Cunningham secures forward contracts and options for milk on the Chicago Mercantile Exchange (CME), and options for corn and soybean meal on the Chicago Board of Trade (CBOT).

Contracts on the exchanges are not connected to physical transactions of milk, corn, and soybean meal. For example, Cunningham’s milk is sold to DFA, priced according to his federal order. With milk trading at $19.00 / cwt, a future contract (or forward contract) on milk at $19.00 / cwt would generate zero return if the price of milk holds precisely at $19.00. If milk falls below $19.00, Cunningham continues to sell milk to DFA according to the price dictated by the federal order, but the value of his forward contract increases. In this way, the lower price he receives according to the federal order is offset by the increased value of the forward contract, thereby resulting in a realized milk price to the dairy of $19.00 / cwt. If his federal order price exceeds $19.00 / cwt, the same forward contract is now a liability, daily marked to market, so Cunningham must maintain enough liquidity in his brokerage account to cover the difference each day. However, as milk is sold to DFA at the higher federal order price, the realized milk price to the farm remains $19.00 / cwt.

AT MILK UNLIMITED DAIRY FARMS, every detail in the parlor reflects a larger commitment — blending hard work, precision, and strategy to secure the future of the herd and the business. (Photo Credit: John Gawley/Standard Dairy Consultants).

At times, Cunningham uses call and put options instead of forward contracts to set a floor and ceiling on his milk price, thereby giving him greater participation in price upside, while restricting downside risk. For example, with milk trading at $19.00, buying a put option (price floor) at $18.75 might cost $0.55, but $0.30 can be recouped by selling a call option (price ceiling) at $20.25. In this way, a price floor and ceiling can be set for a net cost of $0.25. To further decrease the cost of his options trades, Cunningham utilizes a third option leg by selling an in-the-money call.

Importantly, Cunningham never contracts only milk or only feed. To do so would violate the basic tenet of his philosophy, which is managing margin.

Managing margin requires that both sides of the equation- income and expense -be controlled beyond the open market.

In our current market environment, the outlook is excellent for Milk Unlimited. Using a percentile analysis of projected margins to compare his current outlook to previous years on record, Cunningham lights up as he says he is on track to have profitability in the top 25% of his years on record. With this sort of market outlook, why would a manager not want to lock this in?

That was the exact question I asked Cunningham. “Four things tend to stand in the way of producers taking this approach,” he explained:

- They don’t know their cost of production.

- They have a fear of missing out on the top of the market.

- They have previously contracted one side (milk or feed) and lost.

- They have insufficient capital to cover margin calls.

And what about dairies that think they are too small to protect their margins? “That is false,” says Cunningham. “It doesn’t matter about the size of the farm. A very small producer can still forward contract feed and utilize DRP with any amount of milk. Dairy Margin Coverage is a perfect tool for small farmers because the first 5 million lbs. of milk is heavily subsidized.” In addition to the subsidized programs, some primary milk purchasers, such as DFA, also assist dairy farmers with forward contracting of milk price. Cunningham’s response reflects perfectly to his philosophy. Margin protection is far less about the specific tools employed (options, futures, or physical contracts), and much more about knowing the actual cost of production, projecting margin, and taking appropriate steps to cement margin and avoid unprofitable years. This could not be more important than for dairies considering leveraging their current equity positions for growth or generational succession, as the risk of one or two unprofitable years pushes farms closer to exit.

As managers look forward into the second half of 2025 and the first half of 2026 with potential uncertainty, there is a clear resolution. Start by working with your farm advisors to monitor the cost of production and project profitability. Then, take appropriate steps to secure that profitability and protect against downside risk. As Cunningham states, “Consistent, year-over-year profitability is the ideal foundation for sustainable growth.”

Standard Dairy Consultants can help.

We understand you measure our value by the results our people deliver. Our experienced team knows how to apply their knowledge to your specific operation in ways that directly impact your efficiency and performance and, ultimately, your profitability. The only way to be good at what we do is to develop a good working relationship with you. We’re regular fixtures at your farm as we get to know you, your people and your herd.